An SMSF can invest in properties overseas as neither the SIS Act or the ATO prohibit these types of investments. This type of investment is not too different to investing in Australian property.

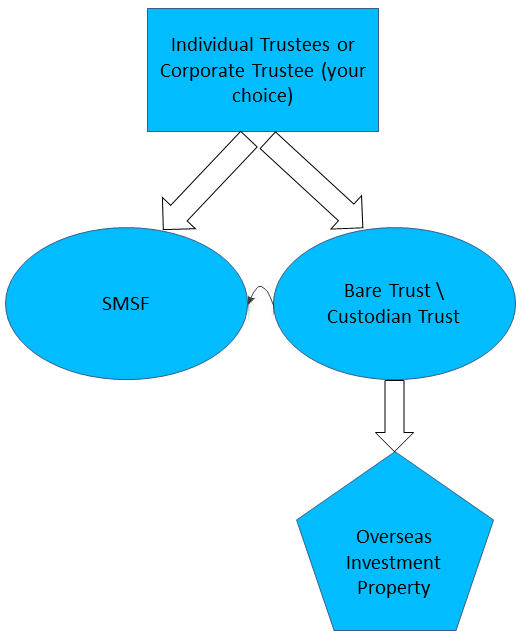

The SMSF must have legal title over the overseas property. Some countries will not allow the SMSF to hold the title of the property. Hence a structure looks like the below graph will need to be set up before the Fund invests in the overseas property:

The above structure is also required if there is borrowing involved in purchasing the property.

Note: The SMSF owns 100% of a Bare Trust \ Custodian Trust. The SMSF has 100% ownership of an overseas investment property and an overseas bank account

There are a number of options and requirements that the fund will have to address before investing in an overseas property.

- The Fund will need to ensure the Investment Strategy and the Trust Deed allows the SMSF to invest in an overseas property.

- An SMSF, although not unique to Australia, may not be recognized in the country you are investing in. If you need, we can establish a suitable structure that will meet the legislative requirements both abroad and in Australia.

- The overseas property will need to be in the name of the SMSF or a Bare/Custodian Trust that the Fund has control over, there are some exceptions detailed in the next point where foreign investors are restricted to buy property.

- In some Asian and sub-continent countries, foreign overseas investors are not allowed to own property. The Fund will need to find a resident (preferably a member of the SMSF) in the country who can represent the fund, so the title of the property can be accommodated in the structure.

- The SMSF needs to make sure that the property has not been used as security for a loan or mortgage.

- The laws and customs are different in all countries and the implications specific to that country will need to be adhered to.

- The entity you have established will have to be registered to pay taxes in the overseas country. An accountant in that country will be able to provide the appropriate assistance. We will be able to help you with the tax obligations locally.

- To avoid paying double taxes here is a list of countries that the ATO has a reciprocal tax treaty with.

- If you are planning to borrow funds to make the overseas property investment, the Fund must confirm that the SMSF loan includes limited recourse arrangements and the correct limited recourse clauses.

- The LRBA terms and conditions must be consistent with good arm’s length practices.

- The SMSF or Bare/Custodian Trust will need to have an overseas bank account to receive rent payments and pay for maintenance and other related expenses. The financial institution will need to meet the definition of a Deposit Taking Institution as stipulated in the Banking Act 1959.

- Where the language spoken in the investing country is not English, we recommend that a translation of all documents, contracts and agreements.

- Be mindful that an additional Bare Trust is required to initiate an overseas bank account to be used in conjunction with an overseas property.

- Auditors are stringent in providing sufficient documentation on overseas property investments. This includes a Title Search to confirm the ownership of the property and whether a loan was taken out on the property. You will also need to revalue the property at the end of each Financial year and provide sufficient documents, which is explained more here.

To see how you can invest in USA Property, please see here.

If you require assistance with foreign exchange when purchasing property overseas, you can use TorFX.

More information on this is explained on our Foreign Exchange page here.

Q & A:

Can an individual who is not a Member or a Trustee in the SMSF, hold ownership of an overseas property on behalf of the Fund?

Yes, a third party can hold the title of the overseas property as long as a Declaration of Trust is set up to reflect that the property being held by the third party is on behalf of the Fund and the ultimate ownership lies within the SMSF.