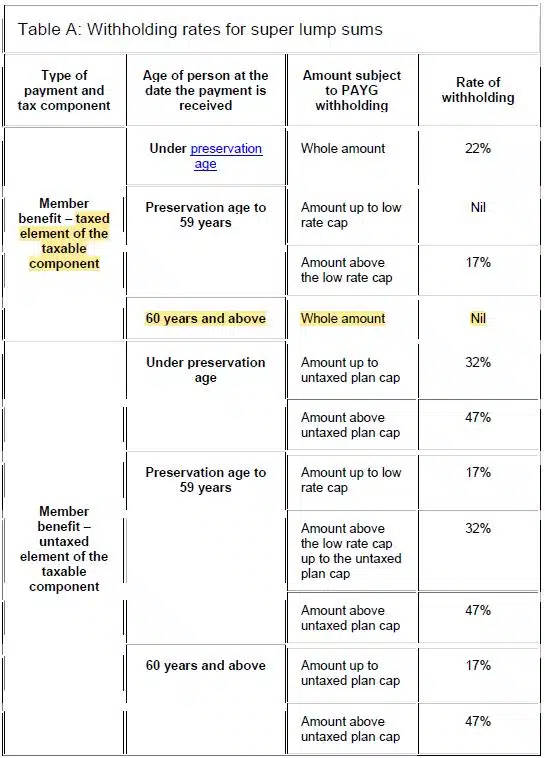

Below is the snapshot of the tax rate table on super lump benefits.

Please also see the ATO website for the Schedule 12 – Tax table for superannuation lump sums.

Lump Sum Paper Work

To withdraw from your super as a Lump Sum, you will first need to determine the components of your super balance. Your SMSF balance may consist of preserved, tax-free, taxable and un-taxed components. Depending on what the tax components are, you may want to consider what the best retirement strategy is for you and your SMSF before you withdraw a Lump Sum. After you have the information required to process a Lump Sum withdrawal or Pension payment, you will need to complete the following:

- Review your Trust Deed to ensure nothing prevents the SMSF from paying a TRIS.

- Prepare a letter from the Member to the Trustee requesting a Lump Sum Pre-payment Statement.

- Complete Part 1 of theLump SumPre-payment Statement. This provides details of the components of the super benefit and gives the Member an opportunity to seek advice regarding the treatment of the payment.

- Arrange for the Member to complete Part 2 of the Lump Sum Pre-payment Statement. Alternatively, the Member can prepare a letter to the Trustee stating how they want to be paid, whether it will be in cash, in specie or both.

- Fill in the PAYG Payment Summary – Superannuation Income Stream form. Once completed, send a copy to the Member with the Lump Sum payment and send a copy to the ATO to be lodged within 14 days of payment. This is not required for Members aged 60 or above as there is no tax payable, unless the Lump Sum is paid from an un-taxed source.

- If the Member is receiving property as part of the Lump Sum payment, then a Minute is required from the Trustee to record this. The Minute needs to record the details of the asset, including the asset’s value and the Minute must record that the asset is being vested to the Member in specie.

- Prepare the accounting records and entries to reflect the Lump Sum payments and ensure the appropriate components are updated in accordance with the proportioning rule.

TBAR Reporting

From 1 July 2018, the Tax Office introduced a new reporting regime for Members with Pension accounts, this is referred to as TBAR. If Members take out a Lump Sum withdrawal, it should be reported to the ATO by lodging TBAR. When instructed, we can lodge a TBAR on your behalf.

Please see our TBAR page in the link below for more detail on the reporting events and times frames.