A Transition to Retirement Pension or transition-to-retirement income stream (TTR or TRIS) is a type of pension from the SMSF that you can commence if you’ve reached preservation age (usually 60) and are still working. With a TRIS you may be able to reduce your working hours without reducing your income. This can be done by topping up your part-time income with a regular ‘income stream’ from your SMSF.

Previously, you could only access your SMSF balance once you turned 65 or retired. This meant it was difficult to reduce your working hours and still maintain a comfortable standard of living. TRIS allows you to withdraw some of your SMSF balance.

Starting a Transition to Retirement (TTR)

You will have two accounts within your SMSF. Once you reach preservation age, you can elect to have a TTR income stream from your SMSF.

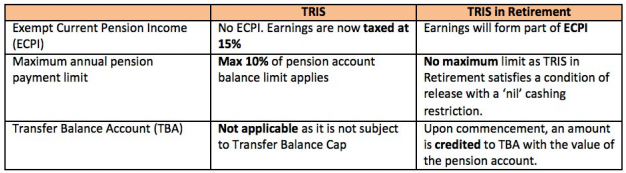

If you elect to start a TTR pension, you can withdraw between the minimum pension percentage and up to 10% of the TTR opening balance for the respective year. The first year of the TTR is calculated on a pro-rata basis, using the days in the year. See an example below:

Example:

A Member reaches their preservation age and wishes to commence a TTR and has $100,000 in their SMSF account. They can withdraw maximum 10% of the TTR opening balance which is $10,000.

Steps to activate a TTR

Step 1: Ensure the Trust Deed has no limitations or prohibitions to start a TTR pension account. TTR pensions were legislated on 1 July 2005. For Funds that were established before this date will require to update the Trust Deed to eliminate the limitation in the original Deed issued at the start.

Step 2: The Trustees of the SMSF are responsible for starting the Transition to Retirement (TTR). When you start a TTR, you must minute your decision (here is a template for these minutes)

Transition to Retirement template

and send a copy of the minutes to Superannuation Warehouse via email if we are looking after your annual compliance.

Tax consequences in the SMSF

Starting from 1 July 2017, all Transition to Retirement income will be taxed at a rate of 15%. This is a new change made in the 2016-2017 Federal Budget.

Tax on the Transition to Retirement income received from the SMSF

If you’re over 60, the income you receive in the form of pension payments from your SMSF is tax free in your hands. If you’re between the ages of 55 and 60, this Transition to Retirement income should be included in your personal taxable income.

Payments cannot be lump sums

You just have to ensure that you withdraw at least the minimum specified percentages as Transition to Retirement payments over the year.

Minimum Drawdown Amount

Depending on your age, you are obliged to withdraw a minimum amount from the Transition to Retirement balance each year. At the start of the year, calculate the market value of the Transition to Retirement. The minimum draw down is dependent on your age. See the preservation age table below for the percentages.

| Age | Minimum % withdrawal for the 2008–09, 2009–10 and 2010–11 income years for certain pensions and annuities | Minimum % withdrawal for the 2011–12 and 2012–13 income years for certain pensions and annuities | Minimum % withdrawal for the 2019-2023 income years | Minimum % withdrawal (in all other cases) |

| Under 65 | 2% | 3% | 2% | 4% |

| 65–74 | 2.50% | 3.75% | 2.50% | 5% |

| 75–79 | 3% | 4.50% | 3% | 6% |

| 80–84 | 3.50% | 5.25% | 3.50% | 7% |

| 85–89 | 4.50% | 6.75% | 4.50% | 9% |

| 90–94 | 5.50% | 8.25% | 5.50% | 11% |

| 95 or more | 7% | 10.50% | 7% | 14% |

Due to COVID-19, the government has halved the percentage of minimum pension payments for the 2022 & 2023 financial years. See here for the current minimum drawdown rates.

During the global financial crisis, the above minimum rates were also temporarily halved for the financial years between 2009 and 2011. This was referred to as minimum pension drawdown relief.

PAYG Registrations

An SMSF must register for PAYG when a Transition to Retirement is started and if the Member taking out pension is less than 60 years of age. You can download the ATO guidance on TTR for SMSF’s below:

Access the ATO website to view the PAYG withholding calculator.

You can view the sample form for the PAYG Payment Summary – Pension Income Stream and the Instruction Guide on how to complete the PAYG form as described by the Tax Office. To download the PAYG Summary – Superannuation Income Stream form, please click here.

You can also view our example for the PAYG Payment Summary and the Calculation for the tax withheld.

More information

To find out more about Transition to Retirement income streams, visit the ATO website by clicking here. Alternatively, you can watch the video below.

-

Q: If I am currently in a TTR, do I need to do another Minute when I enter full pension?

A TTR is distinctly different from a Pension as in the Pension is Tax-free but TTR is not. To start a Pension, there is requirement from 1 July 2017 to advise the Tax Office by lodging a TBAR report. Therefore, to start a Pension, it’s necessary to execute a minute and lodge a TBAR report to the Tax Office. Trustees can either do the Pension commencement themselves or we can assist with it. For more details, please click on this link.

-

Q: I have withdrawn over the 10% maximum limit for TTR, how do I resolve this?

If you have overdrawn over your current maximum limit for TTR you can implement the stop / start strategy. The stop / start strategy works by stopping the current TTR pension and starting a new TTR pension, this process is repeated until the overdrawn amount is rectified.

-

Q: How does a stop / start strategy work?

As an example: If the Trustees of the Fund start a TTR with a balance of $100,000 and the Trustees withdraw $20,000 for the year. This means that they have overdrawn their balance by $10,000, as the maximum withdrawal would be $10,000 (10% of $100,000).

The Trustees of the Fund then decide to commence a stop / start strategy. The Trustees stop their current TTR noting that they have withdrawn the maximum being $10,000. They commence (start) a new TTR with a remaining balance of $90,000, this means that they will be able to withdraw a further $9,000. The remaining balance needed to be corrected is $1,000.

The Trustees of the Fund stop their new TTR and start another TTR noting the current remaining balance as $81,000. The Trustees have rectified the situation but they must still withdrawn the minimum payment for this new TTR being at 4%. This means that the Trustees will have to withdraw a further (81,000 x 4% = $3,240 – $1,000 = $2,240) $2,240 to completely correct the situation.