An Investment Strategy sets out what your SMSF can invest in. When we set up a new SMSF for you, we will issue you with an Investment Strategy Template that you can edit to reflect your choice of investments.

A good Investment Strategy will give your SMSF a wide choice of investment options. SMSFs can generally invest in cash, shares and property, both locally and overseas. SMSFs can also invest in cryptocurrency.Initially, you may decide to invest in cash only and later diversify your investments.

To download a sample of our Investment Strategy template, please click on the button below:

Definition

An Investment Strategy is a detailed financial plan made by the Trustees of an SMSF based on the current and future financial needs of each Member in the Fund. The Funds’ investments must pass the Sole Purpose Test, this means that all investments must be made and maintained on an arms-length basis and that the investment must provide for the Members’ retirement.

Investment Strategy legal requirements

Under the SIS Act, Trustees of an SMSF are responsible and directly accountable for the management of Funds’ Members benefits. Trustees have a duty to make, carry out and document all decisions on how the SMSFs’ assets are invested, they must carefully monitor the performance of the investments. This duty will involve formulating and implementing an Investment Strategy. The Investment Strategy should be reviewed annually or reviewed when new investments are considered, if required the Trustees may wish to update their current Investment Strategy.

The main motivation that Trustees have for setting up an SMSF is “control of investments”. As a Trustee, you are required by law to prepare and implement an investment strategy for your SMSF and review it on an ongoing basis.

The investment strategy must take into account every aspect of the SMSF, including:

- The risk involved in making, holding and realising the SMSFs’ investments, and the likely return from these investments, having regard to the SMSF’s objectives and its expected cash flow requirements;

- The composition of the SMSF’s investments as a whole, including the extent to which the investments are diverse or involve the entity in being exposed to risks from insufficient diversification;

- The liquidity of the SMSF’s investments, having regard to its expected cash flow requirements, for example: payment of tax, the superannuation surcharge liabilities of the members, lump sum benefits if a member leaves the SMSF, and regular pension payments;

- The ability of the SMSF to discharge its existing and prospective liabilities.

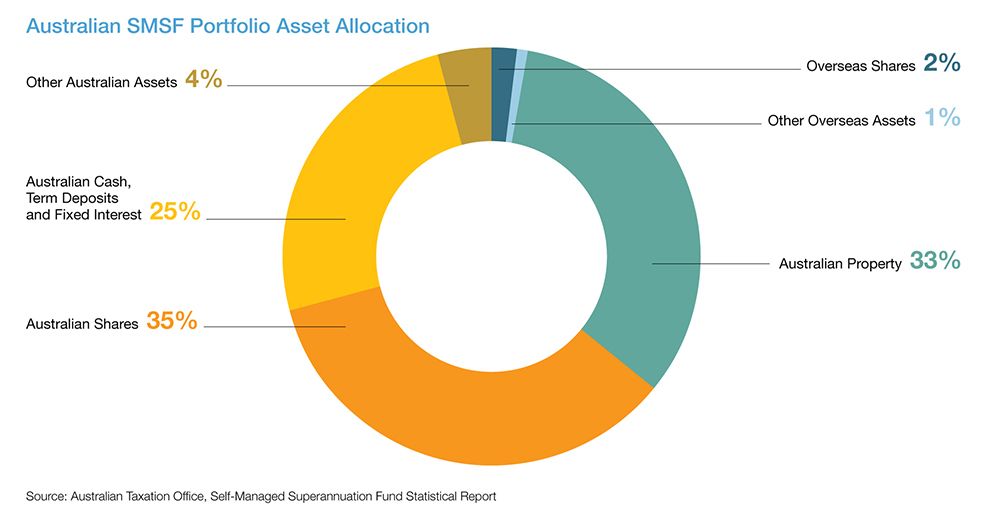

Please see below for a general SMSF Portfolio Asset Allocation.

Investment Objectives, Risk and Diversification

The Trustees of the SMSF may aim to obtain an average yield of their choosing from all investments e.g. 6%. In order to achieve this objective, Trustees should consider the needs of each Member in the Fund. Trustees should also take into account when each Member is due to retire, your risk profile and your growth targets. Generally, risk levels are different for each Member. If Members risk levels are too diverse within an SMSF, they may wish to setup their own SMSFs with other like-minded individuals.

Risk is the possibility of loss on an investment. There is a strong correlation between risk and return. This means that the Trustees must determine the acceptable level of risk and volatility of the returns in the light of the SMSF’s circumstances. Diversification of investments may be desirable in order to disperse and manage risk; it can also reduce the volatility on the return on investments.

Diversification means spreading investments over a number of individual assets, classes of assets, countries, or investment managers. The ATO may contact Trustees to ensure that their SMSFs are appropriately diversified. However, it may be difficult to achieve diversification in the early stages when the amount of funds available for investment may be limited.

Please see below for FAQs about SMSF Investment Strategies

We are Melbourne based with clients throughout Australia. Our SMSF administration service is mostly paperless. This enable us to charge a fair fee, resulting in a good value-proposition for you.

Superannuation Warehouse is an accounting firm and do not provide financial advice. All information provided has been prepared without taking into account any of the Trustees’ objectives, financial situation or needs. Because of that, Trustees are advised to consider their own circumstances before engaging our services.

Follow us:

Shop 1/116 Balcombe Rd, Mentone, VIC 3194

PHONE:

03 9583 9813

0411 241 215

Email:

admin@superannuationwarehouse.com.au

Office Hours:

Monday to Friday

9.00am – 5.00pm

© 2010 - 2024 Superannuation Warehouse : All Rights Reserved

Digital Strategy by